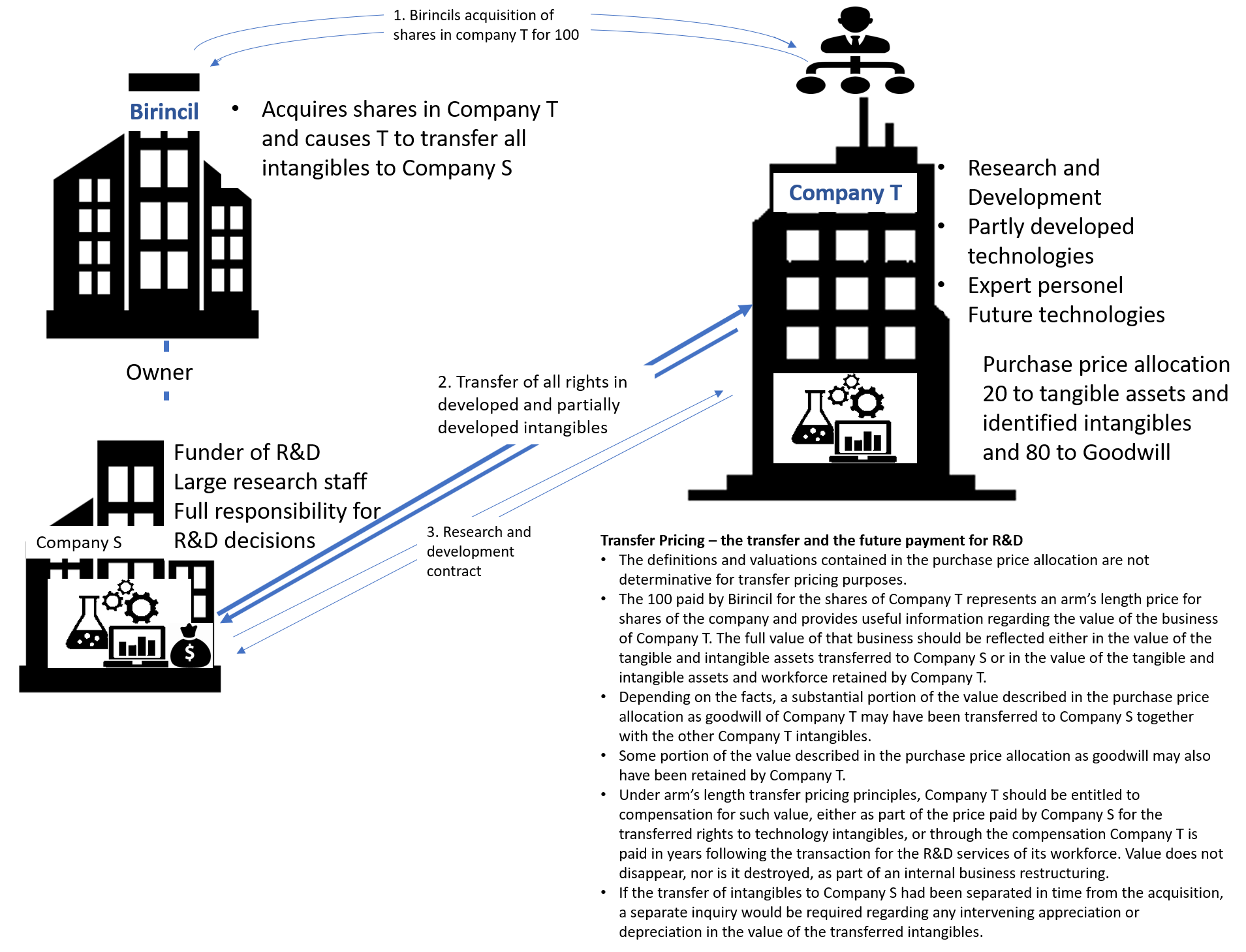

83. Birincil acquires 100% of the equity interests in an independent enterprise, Company T for 100. Company T is a company that engages in research and development and has partially developed several promising technologies but has only minimal sales. The purchase price is justified primarily by the value of the promising, but only partly developed, technologies and by the potential of Company T personnel to develop further new technologies in the future. Birincil’s purchase price allocation performed for accounting purposes with respect to the acquisition attributes 20 of the purchase price to tangible property and identified intangibles, including patents, and 80 to goodwill.

84. Immediately following the acquisition, Birincil causes Company T to transfer all of its rights in developed and partially developed technologies, including patents, trade secrets and technical know-how to Company S, a subsidiary of Birincil. Company S simultaneously enters into a contract research agreement with Company T, pursuant to which the Company T workforce will continue to work exclusively on the development of the transferred technologies and on the development of new technologies on behalf of Company S. The agreement provides that Company T will be compensated for its research services by payments equal to its cost plus a mark-up, and that all rights to intangibles developed or enhanced under the research agreement will belong to Company S. As a result, Company S will fund all future research and will assume the financial risk that some or all of the future research will not lead to the development of commercially viable products. Company S has a large research staff, including management personnel responsible for technologies of the type acquired from Company T. Following the transactions in question, the Company S research and management personnel assume full management responsibility for the direction and control of the work of the Company T research staff. Company S approves new projects, develops and plans budgets and in other respects controls the ongoing research work carried on at Company T. All company T research personnel will continue to be employees of Company T and will be devoted exclusively to providing services under the research agreement with Company S.

85. In conducting a transfer pricing analysis of the arm’s length price to be paid by Company S for intangibles transferred by Company T, and of the price to be paid for ongoing R&D services to be provided by Company T, it is important to identify the specific intangibles transferred to Company S and those retained by Company T. The definitions and valuations of intangibles contained in the purchase price allocation are not determinative for transfer pricing purposes. The 100 paid by Birincil for the shares of Company T represents an arm’s length price for shares of the company and provides useful information regarding the value of the business of Company T. The full value of that business should be reflected either in the value of the tangible and intangible assets transferred to Company S or in the value of the tangible and intangible assets and workforce retained by Company T. Depending on the facts, a substantial portion of the value described in the purchase price allocation as goodwill of Company T may have been transferred to Company S together with the other Company T intangibles. Depending on the facts, some portion of the value described in the purchase price allocation as goodwill may also have been retained by Company T. Under arm’s length transfer pricing principles, Company T should be entitled to compensation for such value, either as part of the price paid by Company S for the transferred rights to technology intangibles, or through the compensation Company T is paid in years following the transaction for the R&D services of its workforce. It should generally be assumed that value does not disappear, nor is it destroyed, as part of an internal business restructuring. If the transfer of intangibles to Company S had been separated in time from the acquisition, a separate inquiry would be required regarding any intervening appreciation or depreciation in the value of the transferred intangibles.