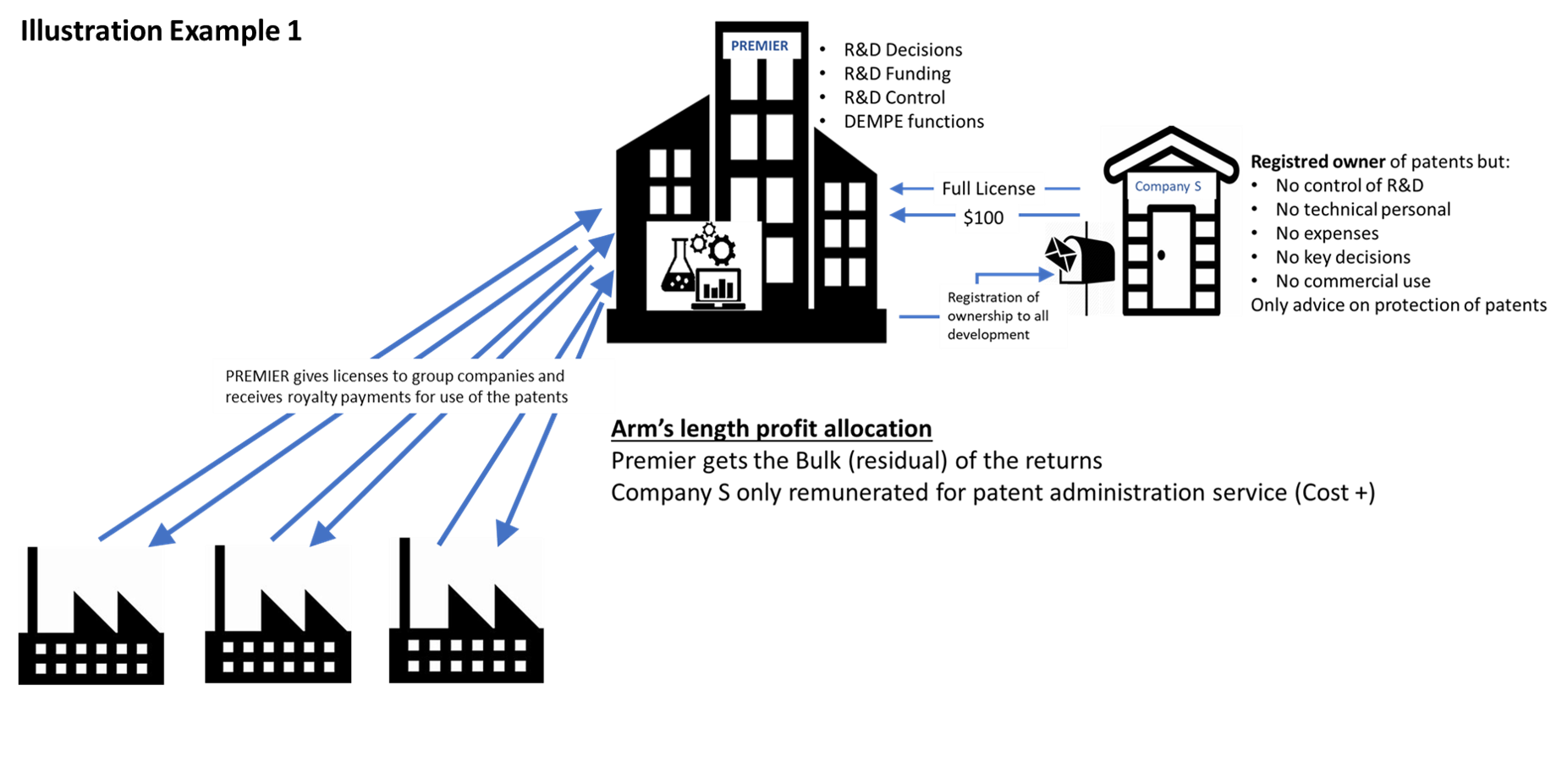

1. Premiere is the parent company of an MNE group. Company S is a wholly owned subsidiary of Premiere and a member of the Premiere group. Premiere funds R&D and performs ongoing R&D functions in support of its business operations. When its R&D functions result in patentable inventions, it is the practice of the Premiere group that all rights in such inventions be assigned to Company S in order to centralise and simplify global patent administration. All patent registrations are held and maintained in the name of Company S.

2. Company S employs three lawyers to perform its patent administration work and has no other employees. Company S does not conduct or control any of the R&D activities of the Premiere group. Company S has no technical R&D personnel, nor does it incur any of the Premiere group’s R&D expense. Key decisions related to defending the patents are made by Premiere management, after taking advice from employees of Company S. Premiere’s management, and not the employees of Company S, controls all decisions regarding licensing of the group’s patents to both independent and associated enterprises.

3. At the time of each assignment of rights from Premiere to Company S, Company S makes a nominal EUR 100 payment to Premiere in consideration of the assignment of rights to a patentable invention and, as a specific condition of the assignment, simultaneously grants to Premiere an exclusive, royalty free, patent licence, with full rights to sub-licence, for the full life of the patent to be registered. The nominal payments of Company S to Premiere are made purely to satisfy technical contract law requirements related to the assignments and, for purposes of this example, it is assumed that they do not reflect arm’s length compensation for the assigned rights to patentable inventions. Premiere uses the patented inventions in manufacturing and selling its products throughout the world and from time to time sublicenses patent rights to others. Company S makes no commercial use of the patents nor is it entitled to do so under the terms of the licence agreement with Premiere.

4. Under the agreement, Premiere performs all functions related to the development, enhancement, maintenance, protection and exploitation of the intangibles except for patent administration services. Premiere contributes and uses all assets associated with the development and exploitation of the intangible, and assumes all or substantially all of the risks associated with the intangibles. Premiere should be entitled to the bulk of the returns derived from exploitation of the intangibles. Tax administrations could arrive at an appropriate transfer pricing solution by delineating the actual transaction undertaken between Premiere and Company S. Depending on the facts, it might be determined that taken together the nominal assignment of rights to Company S and the simultaneous grant of full exploitation rights back to Premiere reflect in substance a patent administration service arrangement between Premiere and Company S. An arm’s length price would be determined for the patent administration services and Premiere would retain or be allocated the balance of the returns derived by the MNE group from the exploitation of the patents.