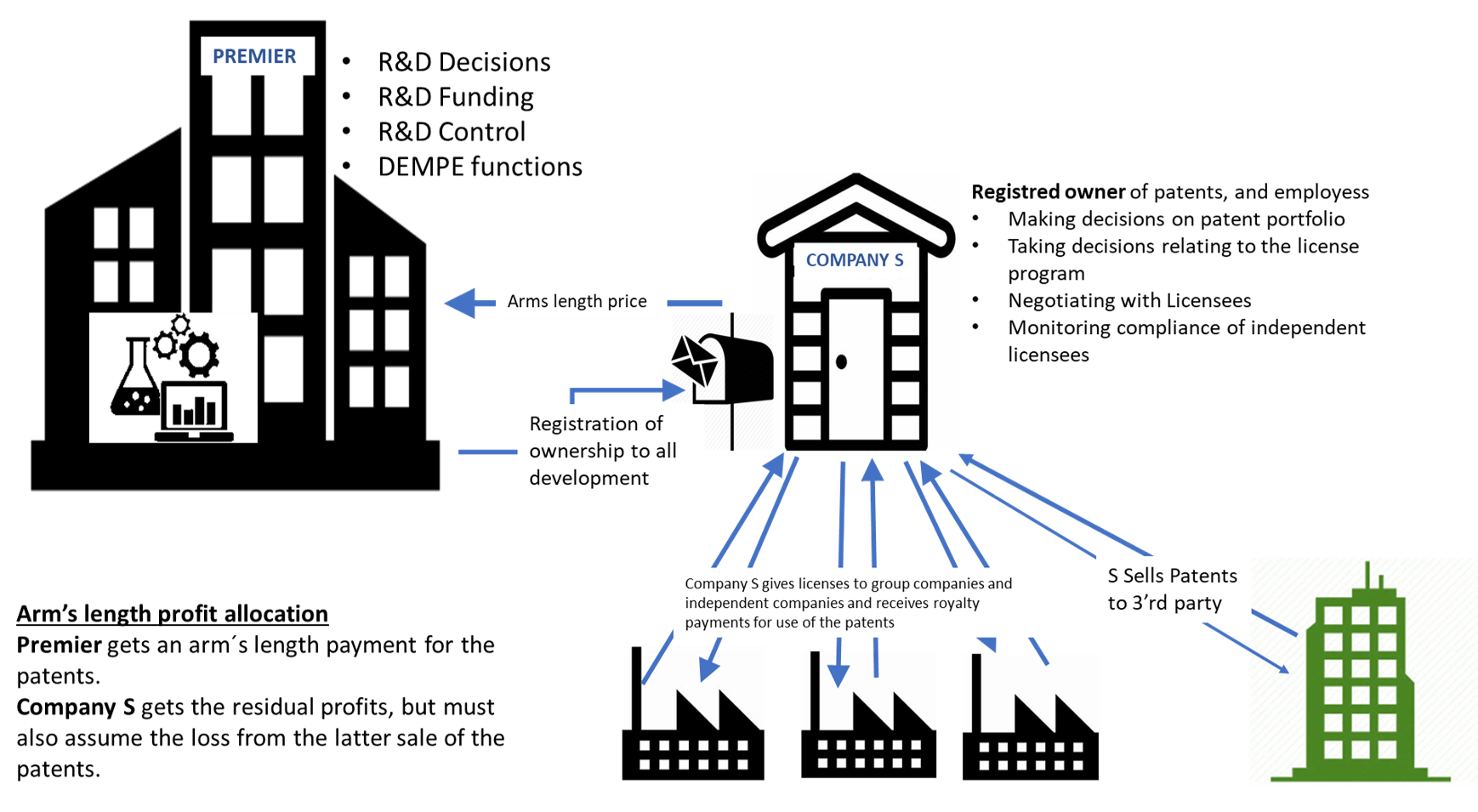

13. The facts are the same as in Example 4 except that instead of appreciating, the value of the patents decreases during the time they are owned by Company S as a result of unanticipated external circumstances. Under these circumstances, Company S is entitled to retain the proceeds of the sale, meaning that it will suffer the loss.